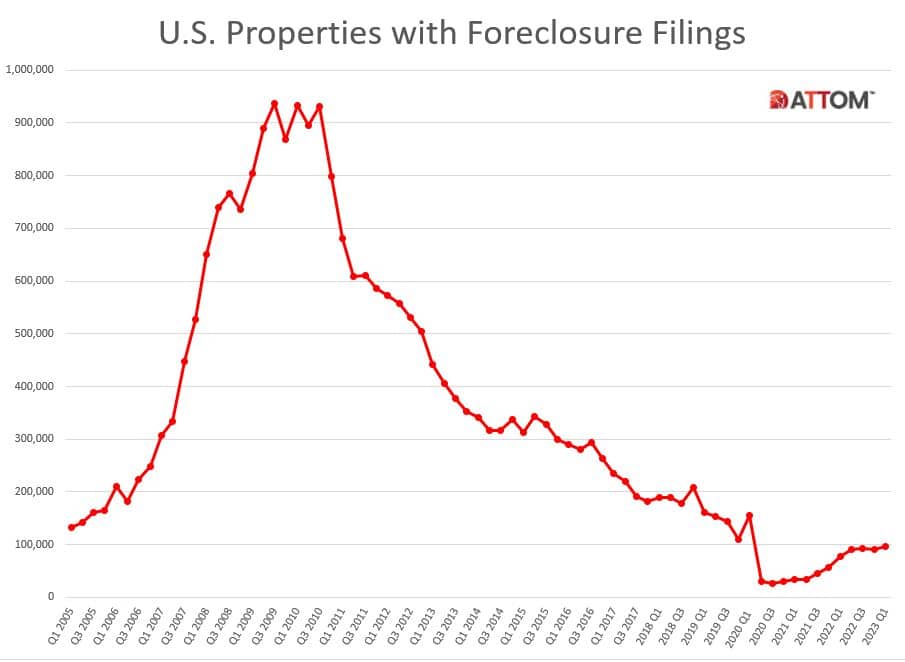

Foreclosure filings in the United States have risen sharply, signaling growing financial strain on homeowners amid high borrowing costs and compounding affordability issues.

According to recently released data from ATTOM, a real estate analytics company, 42,430 properties were foreclosed in April this year—marking an 18 percent increase compared with last year. The spike in foreclosures, which included default notices, bank repossessions, and scheduled auctions, represents a slight dip of eight percent from March but a significant year-over-year rise.

The surge suggests that high borrowing costs and worsening affordability are placing immense financial pressure on U.S. homeowners. Such a spike in foreclosures is reminiscent of the period immediately before the 2008 financial crisis. Completed foreclosures rose by 42 percent annually.

“Foreclosure activity continued its gradual trend higher in April, with both foreclosure starts and completed foreclosures posting annual gains,” said Rob Barber, CEO of ATTOM.

The ongoing rise in foreclosure activity raises concerns about potential cracks in the U.S. economy. Earlier this year, new home sales fell to 587,000 units—a seasonally adjusted figure—the weakest since late 2022 and far below forecasts of around 722,000 units. This plunge by 17.6 percent has prompted President Donald J. Trump to call on Congress this week to pass a Senate bill with explicit restrictions on Wall Street investors buying single-family homes.